Being a one-income household doesn’t mean you have to live paycheck to paycheck. We are a family of 5 living on one income and live comfortably with the help of our family budget. Whether you’re a one-income family due to a stay-at-home parent or a job loss, you can use this method of family budgeting to help you gain control of your finances.

This budgeting advice also works for dual income families and expands on my Budgeting 101 blog post.

Why Budgeting Feels Hard

With inflation, rising housing costs, and child care costs, creating and sticking to a budget can seem out of reach and like it’ll take too much time and is just one more thing on your to-do list.

Guess what though?!

When you learn how to budget correctly and using simple methods that actually work for you, it’ll take you less time in the future AND you’ll be able to cut costs as well as not worry about money, like you are right now.

Know Your Net Monthly Income

The first step is you have to know how much money is coming in every month, a.k.a., your net monthly income from all income sources.

This is the money that actually makes it to your bank account after taxes, deductions, insurance, etc. come out of your paycheck.

Your net monthly income includes your paycheck(s) and any side hustle or side-gigs you have that are consistent.

One caveat here, if you have an inconsistent side gig like I do such as making artwork for others that’s not consistent, don’t include it in your overall budget because you can’t count on that money every month. Instead, it becomes a bonus, in a sense, when you do make those sales.

Track Your Spending

You can do this one of two ways. You can look back at your bank statements and credit card statements for the past month to see where your money has gone, as I detail in my Budgeting 101 blog post, or you can start now and keep track for the next 30 days.

Want bonus points? (ok, there aren’t really points, but stick with me)

Do both! Look back at the past month AND look at this month moving forward.

Separate Fixed vs. Variable Expenses

As you look through your spending over the past month and/or the current month moving forward, you’ll want to categorize your purchases to help you better understand what you’re spending money on.

While you’re doing that, you’ll also want to separate fixed expenses such as rent/mortgage, utilities, insurance premiums, debt payments, student loans, child care,etc.

Then you’ll also look at variable expenses such as groceries, clothing, gas, and kids’ activities. These are all monthly expenses to keep in mind when working with your family finances.

Focus on Essentials

Next, you need to focus on the essentials when it comes to your monthly budget. These include housing expenses, insurance premiums, utilities, child care, food, transport including car repairs, etc.

Then you can tackle debt and putting money into savings.

Common Budget Categories:

- Rent/Mortgage

- Utilities

- Transportation: fuel, car payments, car insurance

- Food/Groceries (essential AND variable expense)

- Insurance premiums: health insurance, life insurance

- Debt payments: student loans, personal loan, car payments (could also go above)

- Savings Accounts: Separate savings accounts for vacation, gifts, vehicle repairs and maintenance, including automated transfers to savings accounts

- Emergency Fund / Emergency Savings Account: great for when unexpected expenses arise

- Kids Activities (variable)

- Daily Needs/Household Expenses: toothpaste, toilet paper, etc. (variable)

Some of these are both essential and variable expenses, depending on the situation. It’s a good idea to look at what you’ve spent in the past, as we did earlier, to see how much you should earmark for each category in your monthly budget.

For example, for our family of 5 living in the Midwest with two of us having food sensitivities, which makes food significantly more expensive, we spend between $1,500 – $2,000 a month on groceries. We don’t eat out at all, due in part to the food sensitivities, that’s all just groceries. We always plan for the $2,000 and if we come in below that, then great, we have extra money!

Don’t Forget Fun!!

Yes, ensuring the essentials are accounted for is an important part of family budgeting BUT you should also earmark some money every month for ‘fun money’/discretionary spending for you and your significant other. If you don’t do this, you’ll just feel really frustrated and burn out quickly.

In our family of 5, my husband and I each get $50 a month to spend on whatever we want. It’s not a lot, but it’s something. It’s nice to still be able to make impulse purchases sometimes while still being well within our budget. If we don’t spend the money that month, we just put that extra money toward our overall end-of-month savings goals.

This helps us have wiggle room, be able to buy what we want within reason, and not feel so restricted.

Granted, if you’re really struggling at the moment with your financial situation, you may want to forgo discretionary spending until your financial situation improves. This is all an ongoing process so just because you need to forgo discretionary spending now, doesn’t mean it will always have to be that way.

How to Cut Costs as a One-Income Family

As you’re looking at your expenses, consider whether you really need everything that you spend money on.

We’ve found that meal planning, cooking at home, not having a home phone or cable television, and cutting hair at home to save hundreds every month.

Here are some ideas for you, we do all of them:

- Meal plan – saves money and food waste

- Cook at home – saves a lot of money and isn’t as hard as it seems (I used to hate cooking but have gotten used to it)

- Cut cable television and streaming services that you don’t really use

- Buy secondhand such as clothing, toys, etc. We do this with our kids and it’s amazing the great things you can get on places such as Facebook marketplace!

- Shop with cashback/reward apps such as Rakuten and Capital One Shopping

- Use local resources that are free such as libraries, parks, and free events instead of paid events

- If you can, do your own minor home repairs

Need More Help?

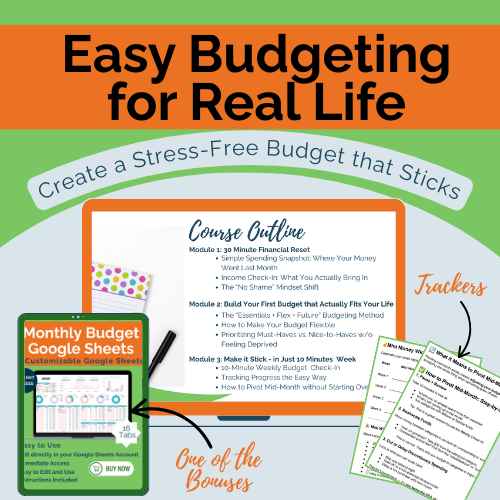

My course, Easy Budgeting for Real Life: Create a Stress-Free Budget that Sticks, will help walk you through seeing where your money is going, building a relastic yet flexible budget that feels good to follow, and how to stick with your new budget using a 10-minute weekly routine.

Bonuses include getting my Google Sheets monthly budget template, mini wins tracker to keep you motivated, and other resources throughout the course to help you get started and stay motivated.

This isn’t some super long course you’ll never complete, all the videos are less than 10 minutes each and are a total of less than an hour. Complete what you can, when you can, and come out with a monthly budget that works for you and is flexible.

What’s Included in the Course

✅ Module 1: The 30-Minute Financial Reset Finally see your financial picture clearly — without shame or overwhelm.

- Simple Spending Snapshot: Where Your Money Went Last Month

- Income Check-In: What You Actually Bring In

- The “No Shame” Mindset Shift

✅ Module 2: Build Your First Budget That Actually Fits Your Life Create a budget you can actually stick to because you created it to fit your own life.

- The “Essentials + Flex + Future” Budgeting Method

- How to Make Your Budget Flexible

- Prioritizing Must-Haves vs. Nice-to-Haves w/o Feeling Deprived

✅ Module 3: Make It Stick — In Just 10 Minutes a Week Learn the weekly routine that keeps you on track (without taking over your life).

- 10-Minute Weekly Budget Check-In

- Tracking Progress the Easy Way

- How to Pivot Mid-Month without Starting Over

🎁 Bonus Downloads:

- Monthly budget template

- Mini wins tracker to keep you motivated

- Resources throughout the course to help you start your budget and stay on track

🎯 Who This Is Perfect For

This course is for you if:

- You feel like there’s never enough money

- You want to budget without stress or shame

- You’re tired of starting over every month and want a system that sticks

- You’re ready to finally feel confident about where your money is going

💸 The Investment

You don’t need to spend hundreds of dollars to get on top of your finances. The introductory price for this course is just $27 — less than one takeout night — and it could change how you feel about money forever.

Even better? You get lifetime access to the course and everything I add to it in the future!

Throughout my parenting journey with 3 kids on a single income, I have become an expert in living comfortably within our means without feeling restricted and I will help you do the same.

I'm a former school psychologist who left my career to stay home with my children, hence the one-income family and needing to adapt to that mentality while still living comfortably.