Are you looking to start budgeting to save money but not sure where to start? It can be overwhelming to do but I’ve got a simple process to get you started on your budgeting journey with Budgeting 101.

Look Back Before Looking Forward

Before you start looking forward, you need to look back to figure out how much you typically spend in different categories before moving forward with creating a budget. This way you aren’t just picking random numbers to plan on each month, you have data to back it up.

1. Gather Statements

The first thing to do is gather bank statements and credit card statements for the past month. You may want to go further back to get a better idea of the average amount you spend but for now, just start with one month so it’s not overwhelming.

You can do this by going to your bank’s website and printing off the statement from last month so you can see the money coming in and going out.

Then go to the website of any credit cards you use and print those statements off as well.

If you don’t have a printer, you could do this on the computer but it’ll be a lot easier if you can print things out.

2. Categorize Purchases

The next thing to do is categorize the purchases on the bank and credit cards statements.

There may be some that are multiple categories, such as a trip to Walmart or Target. If you made the purchase online or still have the receipt, it’ll be easy to split the purchase up by category. If you don’t, just give it your best guess since we’re just gauging averages at this point.

To do this, just write next to each purchase which category it falls into.

Common categories include:

- Income

- Paycheck

- Cash Back

- Side Job or Hobby

- Mortgage/Rent

- Utilities

- Electricity

- Water

- Natural Gas

- Internet

- Cable TV

- Cell Phone

- Trash/Recycling

- Groceries

- Restaurants

- Fuel

- Daily Needs (shampoo, conditioner, toilet paper, cleaning supplies, etc.)

- Clothing

- Kids Items

- Clothing/Shoes

- Toys/Games

- School Expenses

- Extracurricular Expenses

- Subscriptions

- Netflix

- Hulu

- Paramount+

- NFL Network

- Max

- Amazon Prime Video

- Pandora Music

- Spotify

- Gifts

- Discretionary Spending (basically anything that doesn’t fit in a tidy category)

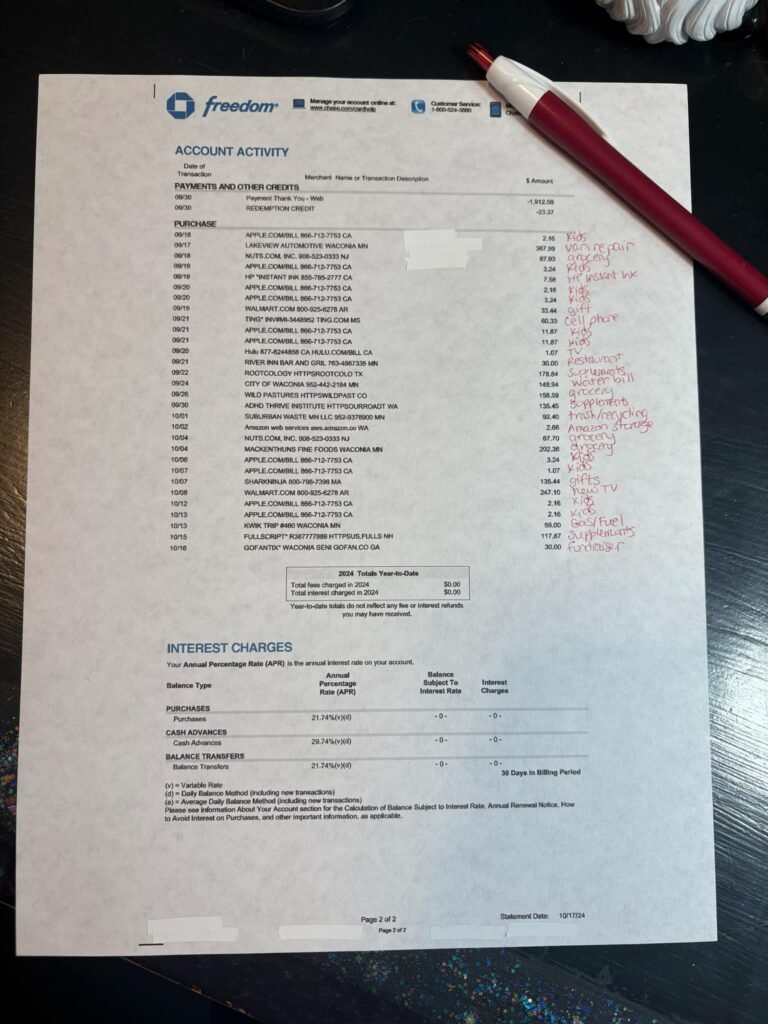

Below is an example of me categorizing one of our credit card statements. Note, there is a new TV on there but we saved up for that new TV and it’s the first TV we’ve purchased in 15 years!

3. Total Amounts for Each Category

After you go through your expenses and categorize them, you’ll add up the transactions for each category.

This will give you a starting point at least based on one month’s expenses on what you’ll want to budget for in the future.

Personally, I’d go back and do this for 3 months to get a good average but it’s up to you. Your budget doesn’t have to be perfect right away, the biggest thing is seeing where your money is going and planning where it’ll go in the future.

4. Reflect on the Data

After seeing how much you actually spend on things every month and what your income is, you can start go see the overall picture of your finances.

Some questions to think about as you look over your data:

- How does this make you feel?

- Are you spending more than you’re making?

- Do you feel secure in how much money is left over every month?

- Do you have any money left over at the end of the month to put in a savings account for unexpected expenses, retirement, or college funds?

5. Set Budget Amount for Month

Based on the data you’ve gathered about your income, expenses, and the answers to the questions above, determine the averages of what you spend on the different categories.

For example, we have a budget of $2,000 for groceries for our family of 5 each month. It’d be less if we didn’t have to all be gluten free but we cut expenses in other areas to help with the large grocery bill.

Each family will have their own amounts for what they spend on things in different categories based on where you live, family size, family circumstances, kids activities, income, and more. There is no right or wrong way to do this, just come up with what fits you best for now.

If you set it and at the end of the month realize it’s not accurate to what you needed to spend that month, then adjust for next month while you just get started here. I don’t suggest doing that more than the first couple months while you’re figuring things out otherwise you’re not budgeting you’re just expanding your budget.

Make sense?

Also, ensure that the amount you plan on spending for the month is LESS than your income. You probably already knew that but just wanted to give that reminder.

6. Moving Forward: Keep Track

Once you’ve set your budget for the month based on what you typically spend in each category, keep those numbers in mind as you make purchases throughout the month.

My husband and I have ‘budget meetings’ twice a month, which I’ll go into in another blog post soon. The mid-month meeting around the 15th we categorize what we’ve spent to make sure we’re still on track for the month. At the end of the month we meet again to ensure that we stayed within budget, put any leftover money into savings, toward the principal of the mortgage, retirement, or kids’ college funds, and plan for the next month.

Typically our budget stays the same from month to month though at times things are different such as when we go on vacation, around the holidays due to gifts (see my Budgeting for Christmas post), and other events throughout the year.

Now you’re on track to have a budget and keep it!

If you’d like some help setting up your budget, check out my monthly budget Google Sheet with instructions and automatically updating sheets from the Transactions log to each month.

If you need more help with budgeting, I made an Easy Budgeting for Real Life course that includes my monthly budgeting spreadsheet that will help you get started budgeting, step by step, while I walk you through it all with videos. It’s much easier than you’d think!

FAQ

How often should you create a budget?

Create a budget to follow for a month and check in on it every other week, at a minimum, to ensure you’re on track.

Over time, you may be able to go longer without adjusting your budget but for us, even 13 years of budgeting under our belts, we still adjust our budget monthly based on different expenses that we expect to pop up such as sports for the kids, lawn care, and more.

Throughout my parenting journey with 3 kids on a single income, I have become an expert in living comfortably within our means without feeling restricted and I will help you do the same.

I'm a former school psychologist who left my career to stay home with my children, hence the one-income family and needing to adapt to that mentality while still living comfortably.