We’ve found that using multiple savings accounts for budgeting makes budgeting and saving so much easier! We can save for bigger expenses throughout the year so we aren’t scrambling for the funds when the event arrives! In this post I’ll walk you through how we do it and what to look out for.

Table of Contents

Multiple Savings Accounts for Future Needs

As I’ve mentioned in a different post linked here, it’s important to have a monthly budget, and saving for larger expenses should be part of that budget.

If you need more help with budgeting, I made an Easy Budgeting for Real Life course that includes my monthly budgeting spreadsheet that will help you get started budgeting, step by step, while I walk you through it all with videos. It’s much easier than you’d think!

That aside, multiple savings accounts can really help when it comes to budgeting for future needs. We have multiple savings accounts that we have money automatically transfer to each month based on the amount we’ve determined we need.

For example, for our gifts savings account, we’ve totaled up everyone we buy for whether that be for birthdays, Christmas, Mothers and Father’s Day, or any gift giving occasion. We have it all in a spreadsheet which we then total up all the money we spent on gifts in a year, divide that by 12, then we know how much we need to put into our gifts savings account each month. We have automatic transfers set up to take money from our checking account into the gifts savings account each month so we don’t even have to think about it. This has helped us immensely as we don’t have to worry if we have enough money for gift giving events, it’s always there in the savings account!

I’ll explain more below and how we use this for things beyond gifts.

What to Have Savings Accounts For

If this sounds great to you, here are some ideas of what you may want to have multiple savings accounts for.

Think about the annual expenses you have, large gift giving events such as Christmas and birthdays as well as any trips you go on.

We have separate accounts for different savings goals including:

- Car Insurance and Tabs

- Gifts, especially Christmas Gifts

- Vacation Fund

- Anniversary Fund

- Monthly Surplus

- Emergency Fund

- College Fund (though those are in 529 accounts)

I’ll go over these in more detail below.

What to Look For with Additional Savings Accounts

When you’re looking to open additional savings accounts, there are some things you’ll want to be on the lookout for, especially if you’re considering switching financial institutions.

- Annual APY (annual percentage yield): These vary from bank to bank and even within the same bank but between different savings account options. You may want to shop around to different financial institutions to see who offers higher interest rates if you feel yours is lower than you’d like. Recently, I was considering whether we should move our emergency fund to one of the local credit unions but found that their annual percentage yield was significantly lower than what we currently have so it wouldn’t make sense to make the switch.

- Minimum Balance Requirements: Some savings accounts have minimum balance requirements, be sure to check this out before opening one. This is especially true when it comes to high-yield savings accounts. It can be worth it for things such as an emergency fund since you’ll hopefully never need to touch that money but always good to know ahead of time what to expect. The last thing you want is to have to pay fees because you didn’t keep up the minimum balance.

- Fees: Be on the lookout for monthly maintenance fees, minimum balance fees, and withdrawal fees. There are plenty of online banks, and probably others, that don’t have these monthly fees. Personally, I won’t open an account with a bank that has a fee.

- Accessibility: Think about how you want to access your money. Do you want to use one of the many online banks or would you prefer a local bank? Or do you want a credit union? This will likely depend on where you already have your checking account but you may find while doing this research that you want to switch that as well. Often, with completely online banks they offer many fee-free ATMs so you can still take cash out if needed.

- Direct Deposit: Some credit unions or banks, especially with high-yield savings accounts will either require direct deposit or give you a higher annual percentage yield if you connect a direct deposit. One of the credit unions I was looking at recently offered an additional 0.25% if I connected a direct deposit that brought in a certain amount of money per month. Since this is for savings accounts, I decided not to do so, but it is an option out there. I could be wrong but I think that if you wanted to do that to take advantage of additional APY you could talk with your employer to have them put a percentage or amount of your paycheck into certain accounts but I’m not completely sure on that as I’ve never been in that situation.

- Transfer & Deposit Options: How easy is it to set up a transfer between your checking account and the savings accounts? For us, it’s just clicking a few buttons online and we’re all set. It’s a good idea to see what this will be like before opening additional savings accounts. It should be easy to transfer funds between accounts, make mobile check deposits, and set up automatic transfers (which I highly recommend).

- FDIC or NCUA insurance: Whenever you’re choosing a financial institution, be sure that they are insured. For banks that means FDIC Insured and for credit unions that means NCUA insured. This way, your money is protected even if the particular financial institution you have it through goes under for some reason.

How to Set Up Multiple Savings Accounts

As I’ve mentioned above, it’s really helpful if you have your additional savings accounts at the same financial institution that you have your checking account at to make it easy to set up additional accounts and future transfers. If not, you could always find another financial institution that does allow this or use a cash system if you tend to buy things using cash.

Depending on the financial institution you go through, you’ll have different options to add different accounts. I can’t go through every bank out there so I’ll just show you how to do it for Capital One banking. Here is the step-by-step process:

1. First, sign in and navigate to your checking account.

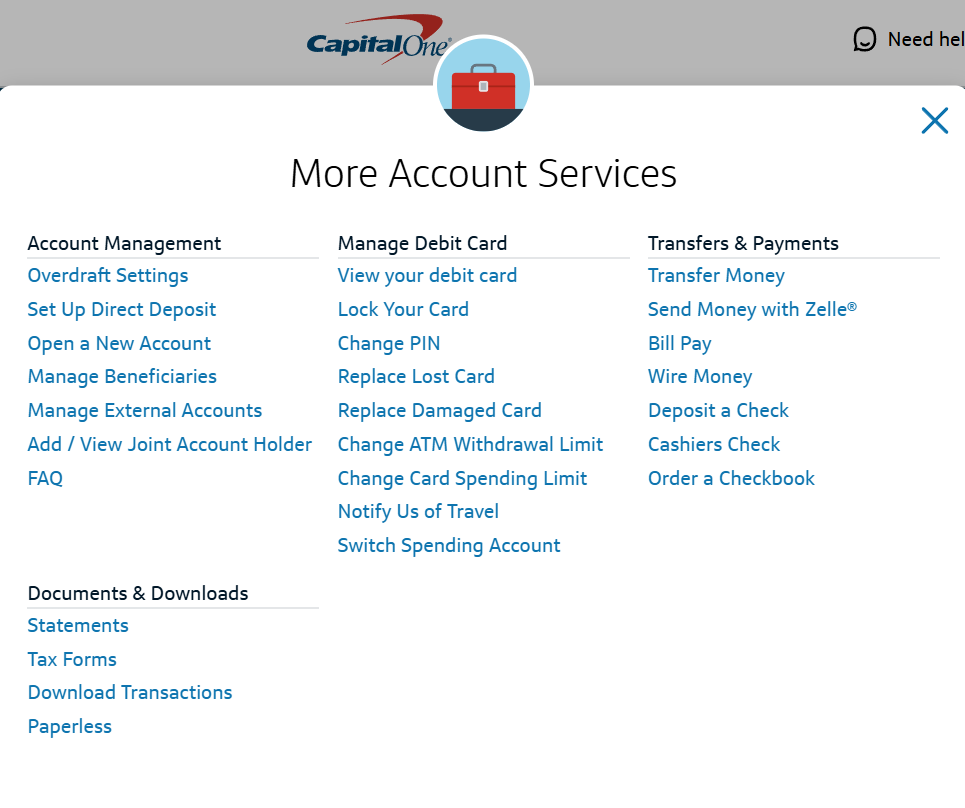

2. Click on more account services and you’ll see the pop up window I have taken a screen shot of above.

3. Then you’ll click on “Open a New Account” under Account Management

4. That will take you to a page where you can click on ‘Savings Accounts’ on the top to see more information about starting a new savings account. For this bank, they have two options, a 360 Performance Savings or CDs. We’ll just stick with the Performance Savings for now, as that’s what I’m used to using.

5. Once you’ve selected to open a 360 Performance Savings account, you’ll be taken to this page where they will help you get started. If you are using the same bank that you already have money in, it’ll be much easier to go through and open additional savings accounts. We have 8 savings accounts and it’s super easy to open more through our online bank.

Often, such as with our bank, you can set up joint accounts. My husband and I have all of our accounts being joint accounts so both have a clear financial picture of what’s going on.

Setting Up Automatic Transfers

To set up automatic transfers from your checking account to additional savings accounts will vary depending on the financial institution. For CapitalOne it’s really simple.

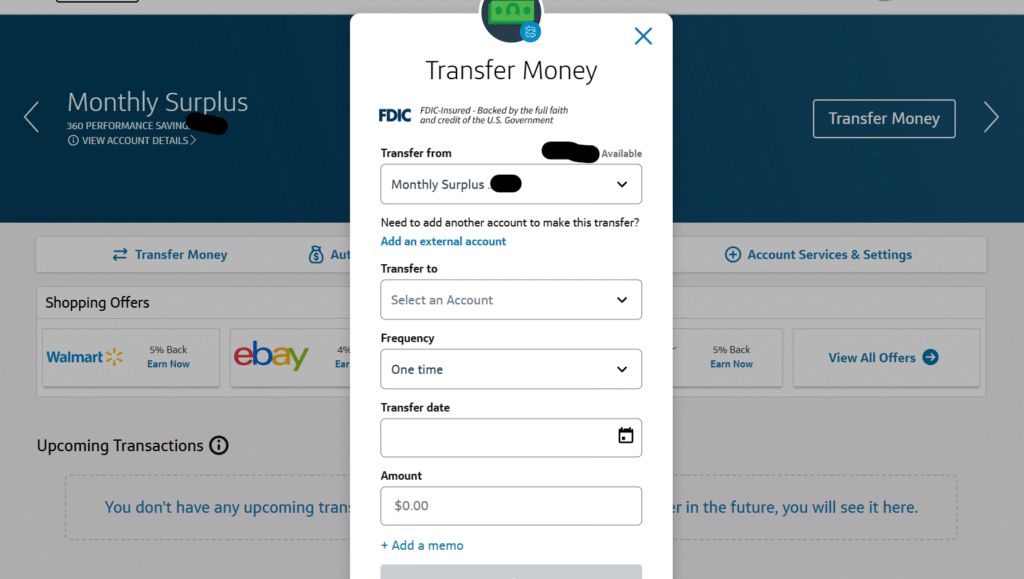

- Select one of your new savings accounts and select “transfer.” Then, the box below will pop up and you can enter in the details.

- Indicate where you want the money to transfer from (probably your main checking account) and which savings accoutn you’d like to transfer it to.

- Check whether you’d like to have this be a one-time transfer or a recurring transfer. We have ours as monthly automatic transfers but it’s up to you.

- Specify the date you want this to start and how much you want to transfer. You can even include a short memo if you’d like.

Again, each financial institution will have different ways to set up automatic transfers. You should be able to find answers on the website of your bank or you can always contact your financial institution to learn more. Hopefully it’ll be as easy with your bank as it is with ours! We don’t need to make life more complicated, we’re trying to make it easier!

How We Use Multiple Savings Accounts

As I noted above, we have many different savings accounts. I’ll go into detail with how we decide what goes into them and why we have them.

- Car Insurance and Tabs: We total up how much the tabs are for our vehicle, car insurance for the year, and expected maintenance such as oil changes. Then we divide that number by 12 to figure out how much to have automatically transferred into our car savings account per month.

- Gifts, especially Christmas Gifts: We do the same for gifts though it’s a bit more complicated since there are many gift giving occasions throughout the year and many different people we buy for. We figure out a budget for each person and each holiday then add them all together and divide by 12 to see how much we have automatically transferred to our gifts savings per month. This is more of a short-term savings account in a sense that this one is more likely to get touched from time to time.

- Vacation Fund: We tend to just take one vacation in the summer plus a camping trip so we only need about $3,500 a year in our vacation fund. We do the same as with the others, total up what we need and divide it by 12. You could also use this to save toward a dream vacation if that’s more your style.

- Anniversary Fund/Surplus: This one is a bit different. We have an amount we spend on each other for our wedding anniversary each year. Often, we don’t spend that whole amount on each other because we just don’t need more “stuff”. Instead of that money going back into the general fund, we put it into our anniversary surplus savings account so if we ever want to go on a trip together, just the two of us, or do something more expensive like that, we’ll have the money for it! Our kids are little at this point so we don’t plan on doing it anytime soon but it’s neat to see that account grow!

- Monthly Surplus: At the end of each month we see how much is left that we didn’t spend and decide where it goes. Typically, the majority of it goes to pay down the principal on our mortgage because that’s our only debt now and we want to get rid of it as soon as we can! Otherwise, we put some money into retirement accounts, on top of what is already deducted from my husband’s paycheck, money into our kids’ college funds, and money into a monthly surplus account that we have available if anything comes up such as the van breaks down, the furnace goes out (we’ve had this happen twice already!), the basement floods, etc. At least we have some money on hand in case it’s needed for any unexpected expenses or home repairs.

- Emergency Fund: This is really important to have. Even just starting out at $1,000 as Dave Ramsey suggests, is a great idea to have a cushion for when unexpected things come up. It’s ideal to have 3-6 months of expenses saved up if you can, but everyone has to start somewhere! I always think about it as what if there was a job loss in our family, what would we need to stay afloat until a new job opportunity arose?

- College Fund: it’s great to have a savings account for a college fund for your kids as well. Personally, we have our kids’ college funds in a 529 account, one for each kid, but it’s up to you how you want to handle that.

Removing Money from Savings Accounts

When it comes to the event, such as a birthday, that you spent money on gifts, all you have to do is transfer the same amount of money from your gift savings account into your checking account and it won’t hurt your monthly budget at all!

You can keep track of how much you spent on each person within a handy spreadsheet like this one or one you create on your own. Be sure to update your goals and savings accounts as your spending habits change.

Misconceptions about Savings Accounts

Some may think that multiple savings accounts are just for the wealthy. I’m here to challenge that belief.

We started having multiple savings accounts back when my husband and I both were employed full time but each made below the average wage in America, even though we were college educated (plus I have two graduate degrees!) Therefore, we were not wealthy when we started this and we still don’t consider ourselves wealthy, especially since we’ve lived on one income for the past 8 years.

In fact, when we didn’t have much money and were saving for a down payment on a house, having additional savings accounts helped us reach our financial goals! We were easily able to keep track of how much we had to go toward our down payment and how much we needed to save each month to reach our goal.

My husband told me that even before then, back when he was single, he had an additional savings account where he was putting away money to save up to buy me my engagement ring! Again, we weren’t wealthy.

Having multiple savings accounts can help you reach different goals by being able to see them more clearly and make better financial decisions when you can easily see where your money is.

Pin for later!

Throughout my parenting journey with 3 kids on a single income, I have become an expert in living comfortably within our means without feeling restricted and I will help you do the same.

I'm a former school psychologist who left my career to stay home with my children, hence the one-income family and needing to adapt to that mentality while still living comfortably.