Are you thinking about leaving your career to become a one income family? I made the leap 8 years ago and we’re living comfortably as a family of 5 on one income, ever since. Here’s what we did before I left my career to ensure we could make it work.

How To Prepare to be a One Income Family

When I decided I wanted to leave my career as a school psychologist over 8 years ago, there were many things we had to figure out before becoming a one-income family.

It can be scary to live on a single income, relying on just one person to carry the financial burden of the whole family. I decided I wanted to leave my career the same month we paid off my graduate school student loans. It was good timing, in a sense, as that was a huge bill every month prior to that. We had been saving money and overpaying on the loans for years to be able to pay them off early.

Here are other things we did/kept in mind:

- Start budgeting before you leave your career to see where your money goes every month and if you can afford to not have your income.

- See what your budget will look like once you don’t have your paycheck, but also keep in mind, the things that you’ll save money on (see below)

- Keep in mind health insurance costs if the person leaving the field is the one who had the family health insurance come out of their paycheck. Find out how much health insurance will be with the person continuing to work’s employer per month plus what the deductible will be. In addition to general health insurance, consider dental insurance and vision insurance, if they are separate policies.

- Medical payments: beyond health insurance, consider medication that isn’t covered by insurance, putting money away in a Health Savings Account (HSA) for medical appointments to cover your deductible, etc.

- Have an emergency fund of 3-6 months income in case something happens to the person who still is working, to give you some wiggle room to get a new job or recover from injury,etc. This can also help with unexpected expenses such as a vehicle breaking down, home repair, increased living expenses, etc.

- Consider your mortgage payment, if you have one, are you on a fixed rate or a mortgage repayment plan that may increase over time?

- Student loan payments: Are they fixed or income-based? Will they increase over time?

- Credit Card Debt: pay off any debt from credit cards, if you have any, before leaving your job.

- Other Debt: pay down or off other debts you have so you have less that you have to worry about each month before you leave your job. These include car payments, a personal loan, medical loans, etc.

- Retirement savings: consider how much you have been putting away from both people’s jobs into a retirement account, and whether you want to keep putting away that much, even when you’re a single-income household. (I suggest that you do, but that’s up to you).

- Grocery budget: Consider how much you spend at the grocery store every month, and whether you think that’ll change in the future.

- Consider other insurance products: these include home insurance, car insurance, an umbrella policy, life insurance, disability insurance, etc. These may change once you become a one-income family, check with your insurance company or agent. One thing to note, if you already have disability insurance as a two-income household, you won’t be able to adjust that policy or renew it for the person who no longer has their own income.

- Other home costs: home costs, including electricity, water bill, gas bill, internet, phone/cell phone bill, trash/recycling, streaming services, etc.

- Consider talking to a financial advisor or other financial professionals, if you have one or want more input, prior to making the switch to get a clear picture of what to expect.

- Baby Supplies/child supplies: such as clothing as they grow, diapers, formula, food, toys, learning resources, etc.

- Consider the future income of each person: At the time that I left my career, we both made the same amount of money at our jobs. However, we knew that with my career in a public school, I wasn’t likely to make much more money than I did at the time. On the other hand, my husband’s income would likely greatly increase over the years, especially if he changed jobs, eventually. Consider who has the highest growth potential in their career, when choosing who is going to leave their job. Of course, also consider who actually wants to stay home with the kids or leave their career. Lucky for us, it worked out that I was the one burnt out in my job, wanted to be a stay-at-home parent, and would make the least amount of money over time.

It seems like a lot, it is a big jump to go from a two-income family to a one-income household. With careful planning, you likely can make it work, depending on your financial situation.

When I became a stay-at-home mom, we carefully considered all of the above, looked at our bank account, considered our financial goals, and thought about it a lot before making the final decision. If you need help with all of that, see the bottom of this post for help!

Financial Pros of Being a One-Income Family

Though your family will be bringing in less income, there are some financial pros in being a stay-at-home parent.

Childcare Costs

When I left my career, we only had one child, but even then, that meant $1,300 a month for his care while I was at work (this was 2017, prices have likely increased now),. That was over one of my paychecks at the time, after health insurance, taxes, etc. were taken out. Keep in mind, I had two graduate degrees…and I was making $55K after 7 years in the field.

All that aside, not having to pay for child care was a huge cost savings for us. This could also include nanny costs, childcare pick up costs, after-school care, etc. Once we had twins, I knew the daycare costs of having 3 kids under 3 would not be doable, so my decision to leave my career was set in stone!

Commuting Costs

If you commute to work, there are some savings you’ll have from leaving the field. I used to commute 30 minutes each way, every day, which led to a lot of fuel and regular car maintenance costs. Insurance costs may also go down once you’re driving less.

Depending on where you live or what you plan on doing, you may be able to become a one-car household. We made that switch once my husband started working from home 6 years ago. We didn’t need to do so, but it saves a lot of money in the long run.

If you currently use public transportation, those costs will decrease as well once you’re not commuting to work.

Restaurants

If the person leaving their career used to go out to eat often, you’ll save money now that they are eating at home (at least most of the time). This could also include if you used to take clients out to lunch, or simply didn’t have the time to prep food at home before work, so you tended to get fast food.

Personal Care

If you worked in a job where you felt the need to buy new clothing often, get fancy haircuts, dry cleaning, or other services, then you leave that career, you may be able to save money by no longer doing those things once you leave.

Work-Related Expenses

Work-related expenses such as continuing education credits, professional development, licensing costs, uniforms, protective gear, and other work-related expenses, depending on your current job.

Need Help Budgeting?

If you need help budgeting, I have budgeting Google Sheets/spreadsheets that can help you, as well as a very low-cost course that will walk you through how to budget.

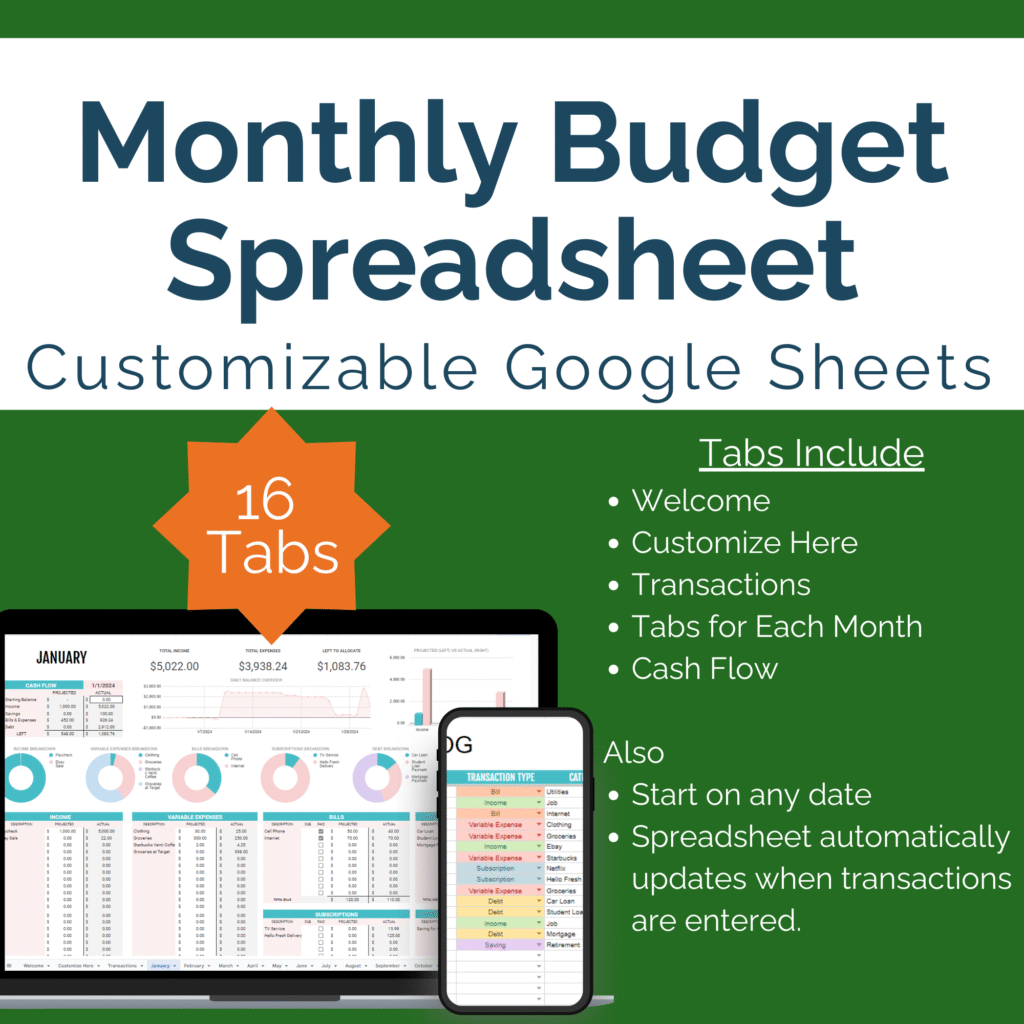

Monthly Budget Spreadsheet, Google Sheet

The monthly budgeting spreadsheet is exactly what we used when we decided we were going to become a one-income family. Just enter your income and expenses for when you’re a two-income household, then in another tab, enter what it’ll be like when you’re a one-income household.

Need help budgeting? The Monthly Budget Spreadsheet is a Google Sheet that we used when I decided I wanted to leave my career. This is where we looked at all of our expenses, and figured out if we could make it work.

Need Help Learning How to Budget?

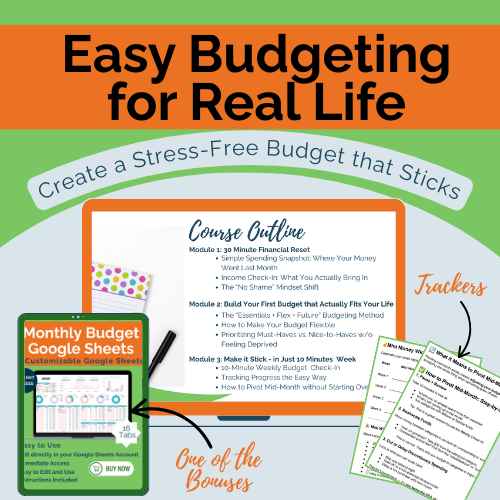

My Easy Budgeting for Real Life course will walk you through how to start budgeting AND includes the monthly budgeting spreadsheet, plus trackers that will help you not only start budgeting, but continue it! Get it at it’s introductory price and have lifetime access so you can keep coming back to it AND get any upgrades that I add to it!

Ditch the budgeting overwhelm and start using a simple, real-life money plan that works- even if you’re on one income, like we are!

A quick-start course to help you stop living paycheck to paycheck — without feeling broke or restricted.

This isn’t another complicated system or guilt-heavy lecture. This is a short, doable, no-fluff course that shows you how to:

- Get clear on where your money is actually going

- Build a realistic, flexible budget that feels good to follow

- Stick with it using a 10-minute weekly routine

- Includes the Monthly Budgeting Google Sheet and additional trackers

- Lifetime access and all future updates included!

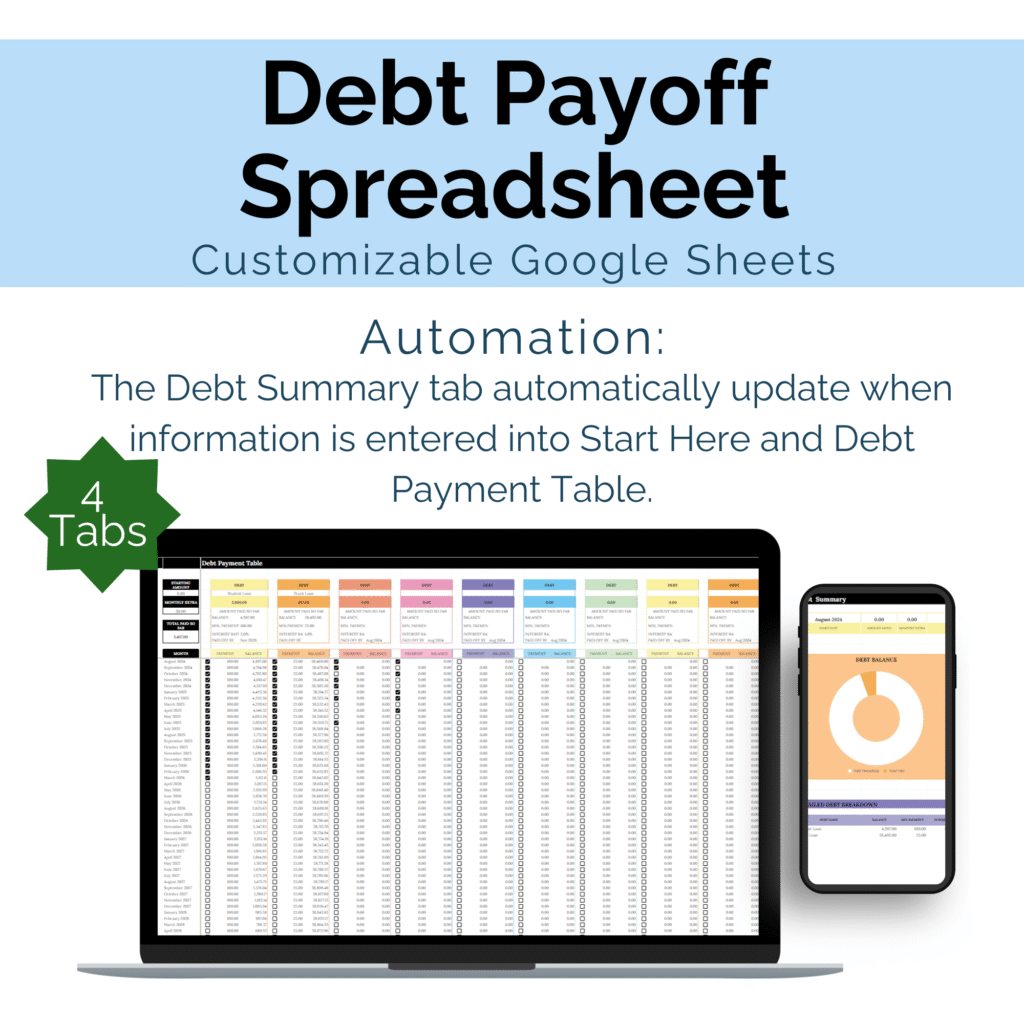

Need help paying off debt?

My Debt Payoff Spreadsheet is a customizable Google Sheet that will help you organize your debt and figure out how to pay it off over time.

Throughout my parenting journey with 3 kids on a single income, I have become an expert in living comfortably within our means without feeling restricted and I will help you do the same.

I'm a former school psychologist who left my career to stay home with my children, hence the one-income family and needing to adapt to that mentality while still living comfortably.